Prediction markets are financial platforms where participants trade contracts linked to future events, with prices reflecting collective probabilities. While these markets efficiently aggregate information, systematic inefficiencies create trading opportunities. Notable strategies include inter- and intra-market arbitrage, exploiting price differences across platforms or mispricing within a single market. Behavioral biases, such as the longshot bias, lead traders to overvalue underdogs and undervalue favorites, while bookmakers may manipulate odds to mislead naive participants. Experienced traders can exploit these patterns to secure profits. This article reviews common systematic edges in prediction markets, illustrates their practical application, and highlights the potential for profitable trading.

Introduction

Prediction markets are financial platforms where participants trade contracts tied to future events. For example, “Will the Democrats hold the Senate after the 2026 midterms?” Each contract typically has two sides, Yes and No, and pays out 1 USD if the event occurs or nothing if it doesn’t. The market price of the “Yes” contract, say, 0.63 USD, can be interpreted as the collective probability (63%) assigned by traders to that outcome.

These markets function much like binary options, but instead of being driven by company earnings or macroeconomic data, they reflect public expectations and private information about political, social, or even cultural events. Because every trader has an incentive to be right, prediction markets tend to aggregate information efficiently, often outperforming polls or expert forecasts.

Interest in prediction markets has been steadily growing, especially around election cycles. After the recent U.S. presidential race, platforms such as Polymarket, Kalshi or earlier projects such as PredictIt saw record participation and liquidity. With the 2026 U.S. Senate elections approaching, activity is expected to increase again, as political analysts, journalists, and even ordinary investors turn to these markets to gauge the real-time odds of partisan control.

The underlying mechanism is simple. Markets transform collective beliefs into prices. A tighter spread indicates higher confidence, while wider spreads signal uncertainty or limited liquidity. Though transaction costs and regulation still limit retail participation, the growing visibility of these platforms suggests they are becoming a legitimate alternative source of probabilistic insight.

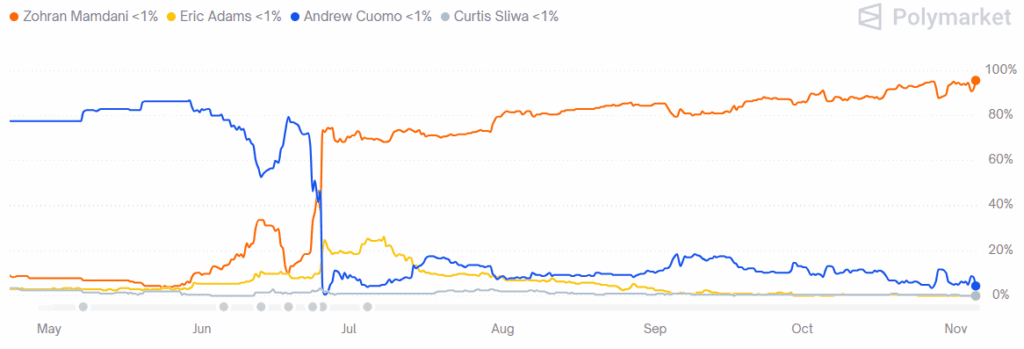

Let’s illustrate the main principle with a simple example. Consider the New York City mayoral election and the winning probabilities of four candidates – Zohran Mamdani, Eric Adams, Andrew Cuomo, and Curtis Sliwa, between May and November 2025. Each candidate had their own token or contract, for example: “Zohran Mamdani wins the NYC Mayoral Election 2025.” The evolution of these probabilities on Polymarket is shown below.

As we can observe, Mamdani’s chances were initially below 5%, then began rising sharply in June and stabilized above 80% from July onward. By late October, his probability of winning was nearly 100%, indicating that the market ultimately priced him as the overwhelming favorite. Andrew Cuomo experienced a completely different trajectory. At the beginning of the observed period, he was the leading candidate until June, when his chances dropped significantly and have not exceeded 20% since.

This situation has the following implications for traders. As mentioned earlier, the price of each contract ranges from 0 to 1 USD, which is interpreted as a probability (0% to 100%). During the market’s lifetime, traders buy and sell these contracts based on new information, causing prices to change in real time, as shown in Figure 1.

Now that the official election results are known, the market has settled. Since Zohran Mamdani won, his contract paid out 1 USD. For example, if you had invested in his winning token 10 times when his chances were 30%, paying 10 × 0.30 USD = 3 USD, you would receive 10 × 1 USD = 10 USD, earning a profit of 7 USD. If he had lost, the contract would have paid out 0 USD, and you would have lost your 3 USD investment.

Similar to other investment tools, trading on prediction markets can also be analyzed and strategized to achieve higher profits. In this article, we will present the most common systematic edges in prediction markets, explain their underlying principles, and show specific applications of these approaches.

Systematic edges

The aim of this paper is to present several trading approaches used in predictive markets in order to develop the most effective and profitable investment strategy. To achieve this, we have reviewed several studies focusing on this field and summarized them in a single work to make the topic more accessible to interested traders. In the following sections, we will gradually introduce the most well-known patterns.

Arbitrage

Looking for an arbitrage opportunity is a longstanding approach not only in predictive markets, but also in equities, futures or other developed market. However, in mentioned areas is not that easy to apply arbitrage as the markets are already well-developed and established, while predictive markets have existed for a relatively short time and their inefficiencies, which typically create arbitrage opportunities, are not yet well captured. This category includes both inter-exchange and intra-exchange markets.

Inter-exchange arbitrage

Inter-exchange arbitrage opportunities arise when the same event is priced differently across multiple platforms. The main idea is to capture the right moment by buying a contract on the platform where its price (implied probability) is lower and selling it where the price is higher. The difference between these prices is referred to as the inter-exchange spread and typically exists only for a short period due to the rapid reactions of market participants.

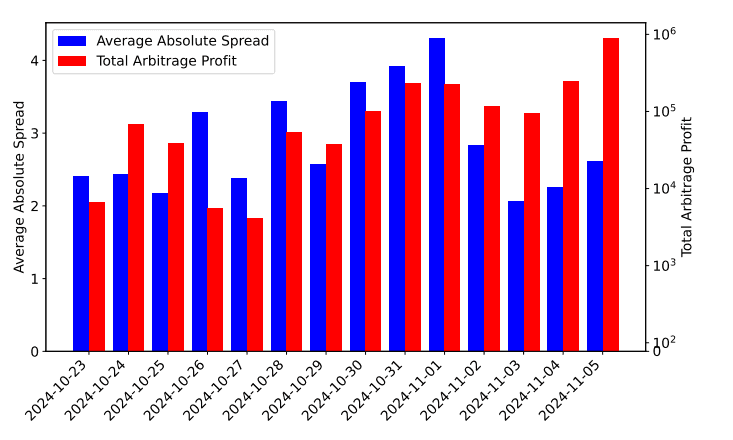

One of the recent studies analyzing inter-exchange arbitrage is Price Discovery and Trading in Prediction Markets. This paper primarily focuses on political events and compares contract prices across several platforms, specifically Polymarket, Kalshi, and PredictIt. The methodology is straightforward. The prices of the same contracts on different markets are converted into probabilities. When the sum of the probabilities of opposing positions on different markets is less than 1 minus the transaction costs, it indicates an arbitrage opportunity.

Figure 2 shows the discrepancy between Kalshi and Polymarket, in terms of both absolute price spread and potential arbitrage profit. The original figure is Figure 6 in the study.

The study also finds that Polymarket generally leads Kalshi due to its higher liquidity, making it particularly informative in the last hours before market closing. However, these arbitrage opportunities typically exist only for a few seconds, at best a few minutes, and transaction costs significantly reduce the potential profits.

Into this category, we can also include the study Unravelling the Probabilistic Forest: Arbitrage in Prediction Markets, published in 2025, although it does not represent a typical inter‑exchange example. This paper examines when arbitrage arises and whether it is present on Polymarket across several dependent markets. Therefore, it is not a standard inter‑exchange arbitrage case, as it focuses on a single platform, but considers different dependent markets within it. The main disadvantage of this approach is that it is not sustainable due to the unpredictable occurrence of arbitrage opportunities, which usually exist only briefly. Moreover, the authors note that liquidity and profits are lower compared to typical inter‑exchange arbitrage. How this mechanism works will be explained in the following section.

Intra-exchange arbitrage

In contrast to inter-exchange arbitrage, intra-exchange arbitrage focuses on arbitrage opportunities created by mispricing within a single market. As mentioned earlier, the prices of the contracts represent probabilities, so the sum of all contract prices should equal 1 USD (100%).

However, sometimes contracts are incorrectly priced, and the sum of the prices deviates from 1. When the sum of all contract prices is less than 1, a buy-all arbitrage opportunity arises. A trader can buy all contracts for less than 1 USD, say 0.95 USD. No matter which contract wins, the trader will receive 1 USD, since the winning contract is included. Therefore, by paying 0.95 USD and receiving 1 USD, the trader secures a risk-free profit of 0.05 USD.

Conversely, when the sum of all contract prices is greater than 1, a sell-all arbitrage opportunity occurs. In this case, the trader can sell one unit of each contract for, say, 1.05 USD in total. Eventually, they will need to pay out 1 USD to the holder of the winning contract, resulting in a risk-free profit of 0.05 USD.

In both situations, the arbitrage stems from the fact that contract prices do not perfectly align with the payout structure, allowing traders to exploit temporary inefficiencies in the market.

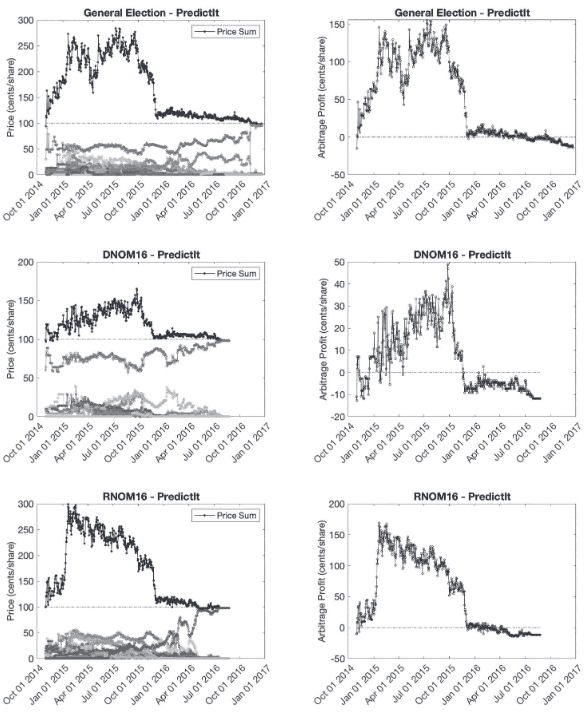

The type of sell-all arbitrage is present in politics ass well. Study Arbitrage in Political Prediction Markets, published in 2020, presents mispricing in PredictIt and IEM during 2016 U.S. election, focusing on Democratic nomination, Republican nomination and general election. At PredictIt market the sum of all contracts was often bigger than 1 USD mostly from 2014 to 2015. Then PredicIt introduced linked markets and profit fees which repeared the wrong pricing.

Despite the 2015 regularization, arbitrage remained sufficiently profitable. Market inconsistencies created opportunities of up to 0.55 USD per contract, representing a 55% profit. In contrast, the IEM market did not exhibit such efficient arbitrage opportunities. Similarly, during the subsequent 2020 election on PredictIt, the profit from this approach was notably lower than in the previous election cycle.

The study Unravelling the Probabilistic Forest: Arbitrage in Prediction Markets also examines intra-exhange arbitrage opportunuties focusing on Polymarket between 2024 and 2025, covering not only political events but also sports events. Other notable publications on the topic include Election Arbitrage During the 2024 U.S. Presidential Election, which specifically examines arbitrage opportunities in the 2024 U.S. election markets.

Longshot bias

Another systematic edge observed on prediction markets is longshot bias. This strategy falls under behavioral effects, meaning that contract prices are influenced by human factors such as beliefs and decision-making. Longshot bias is a psychological phenomenon that occurs when traders overpay for underdogs, hoping for a larger payoff with lower investment if the unlikely outcome occurs, even though the actual probability is low. On prediction markets, where prices are determined by people and their bets on events, this often results in some contracts being overvalued relative to their true chances.

However, in this scenario, it is more effective to invest in the real favorites due to their higher probability of winning.

One of the study examing this bias is Biases in the Football Betting Market published in 2017. Authors analysed 12 084 sport matches from February 2017 to May 2017 and showed that average profit after betting on favorites was -3.64%, while average profit after betting on outsiders was -26.08%.

Not only other traders can create bias, but also bookmakers themselves. The study The Favorite-Longshot Midas, published in 2020, demonstrates how bookmakers deliberately manipulate morning-line odds to mislead naive traders into believing that underdogs have a higher probability of winning. The main objective of this strategy is to minimize the amount of money paid out to winning bettors. However, skilled traders are often able to recognize who the real favorite is and who is merely a “bait” intentionally set by the bookmakers.

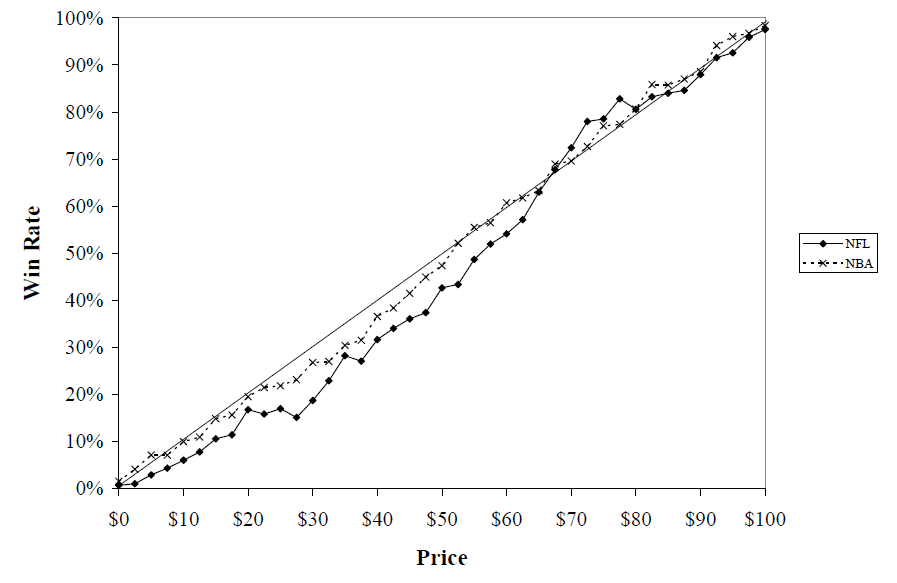

Another study focusing on longshot bias is for example Price Biases in a Prediction Market: NFL Contracts on Tradesports (2007) aimed at NFL contracts.

price level (grouped into $2.50 bands). A win is defined as expiry at $100. .

A similar trend is observed not only in prediction markets but also in stocks and ETFs, known as the lottery effect. This effect reflects that the market is dominated by retail investors favoring underdogs, while there is insufficient professional capital investing in the “boring” but profitable stocks. As a result, underdogs tend to be overpriced and favorites underpriced.

Other

There are, of course, many other profit-boosting approaches in prediction markets that are not included in the previous categories.

For example, study Predictive Power of Information Market Prices (2011) presents a simple trading strategy based on observing the trading process in the prediction market.

On the other hand, if you want to place a bet but lack experience, you might be interested in the BetAI application, which is designed to collect and analyze relevant data to help you determine which contender has the highest probability of winning. More information can be found in the paper BetAI: a Web3-Native Platform for Prediction Markets, AI Agents, and Real-World Asset Ownership.

Prediction markets are not as popular as other investing fields like stocks, therefore availibity of studies and researches is not ideal and sufficient. However, our team will do the best to keep you updated in this topic.

Conclusion

Prediction markets offer unique opportunities for informed traders to exploit systematic edges such as inter- and intra-market arbitrage and behavioral biases like the longshot bias. While these markets efficiently aggregate information, temporary inefficiencies and mispricings create potential for profitable trading strategies. Compared to more established investment fields such as stocks or ETFs, prediction markets are still relatively niche, and the availability of comprehensive studies and research is limited. Nevertheless, they continue to provide valuable insights into collective expectations about future events. Our team will strive to keep you updated on developments in this area and provide guidance as research and market practices evolve.

Author: Sona Beluska, Junior Quant Analyst, Quantpedia

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube