Gold has been in the headlines lately as it climbs to new highs, prompting many investors to look for ways to benefit from the rally. However, many institutional investors – such as mutual funds and pension funds – face restrictions on buying physical gold or gold-backed ETFs. Instead, they often turn to gold mining stocks to gain indirect exposure to gold’s price. That approach seems logical on the surface: mining stocks typically offer leveraged exposure to gold’s movements. But as highlighted by Dirk G. Baur, Allan Trench, and Lichoo Tay in their recent study “Gold Shares Underperform Gold Bullion”, this strategy can be misleading. The authors demonstrate that, over the long run, gold mining shares structurally underperform physical gold itself.

Why the gap exists? The research shows that while gold mining companies benefit from operational leverage – rising more than gold in bull markets – they also carry extra baggage: equity market risk, debt, environmental liabilities, and the finite life of their mines. Because reserves are constantly depleted, miners must reinvest heavily in exploration or acquisitions just to maintain their production levels. These costs erode long-term returns, and their exposure to broader equity market downturns makes them less effective as a hedge during crises.

For investors hoping to mirror gold’s performance, the findings are sobering. Portfolios of gold mining stocks or ETFs like GDX often lag behind gold bullion or gold-backed ETFs (such as GLD), especially over multi-year horizons. While some individual miners may outperform thanks to unique discoveries or operational efficiency, the diversification within a mining-stock portfolio tends to dilute those winners. Thus, unless investors have the skill to identify select outperforming miners or to time gold bull markets perfectly, direct exposure to gold remains the more reliable choice.

Key Takeaways

- Over the 2006–2025 period, the gold miner ETF (GDX) underperformed the gold bullion ETF (GLD) by about –350% cumulatively (≈ –6.5% annually).

- Underperformance is most pronounced over long horizons, during equity market crises, and in gold bear markets; it is only marginal in gold bull markets.

- The main structural reason: finite mine life – miners must constantly replace depleting reserves, which consumes capital and reduces returns.

- Mining stocks are more volatile than gold bullion (about twice as volatile) and often decouple from gold during crises, tracking equity markets instead.

- A few individual mining firms outperform gold, but portfolios/ETFs diversify away that upside, offering little advantage over direct gold exposure.

Authors: Dirk G. Baur, Lichoo Tay, and Allan Trench

Title: Gold Shares underperform Gold Bullion

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5362671

Abstract:

This paper studies the performance of gold miners relative to gold bullion. Gold miners provide leveraged exposure to gold and additional exposure to equity and mining-related risks. On average, miners underperform, especially over long horizons, during crises and in gold bear markets, with only marginal underperformance in gold bull markets. The underperformance is due to finite mine lives which implies that miners must continually replace the gold that they mine with new reserves to match the returns of physical gold. While a selection of gold mining firms outperform gold bullion, a portfolio of gold miner shares diversifies away the idiosyncratic upside of individual miners and is a less attractive investment compared to a direct holding in gold bullion.

As always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

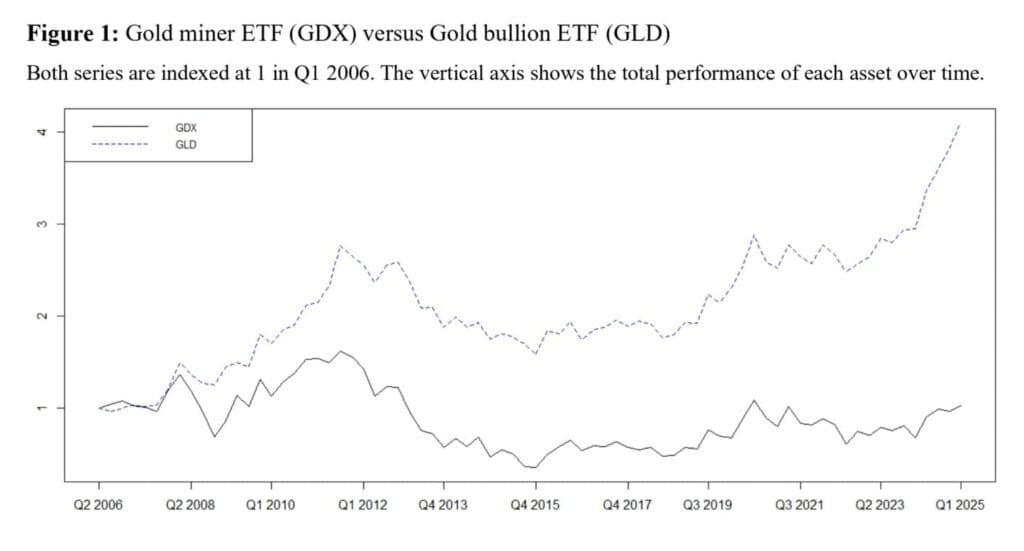

“Figure 1 indicates that gold miners, as represented by a portfolio of gold mining companies (ETF GDX), underperformed gold bullion (ETF GLD) by about – 350% over a 20-year period or -6.5% annually, from 2006 – 2025. GDX’s total return over that period was 26%, and GLD’s total return over that period was 373%. The corresponding annualized returns are 8.1% and 1.2%, respectively.

Figure 1 also indicates that the underperformance is more pronounced in the first half of the sample until 2015 and weaker in the second half of the sample. Indeed, gold miners underperformed by about -120% in the first half and outperformed by about 60% in the second half.

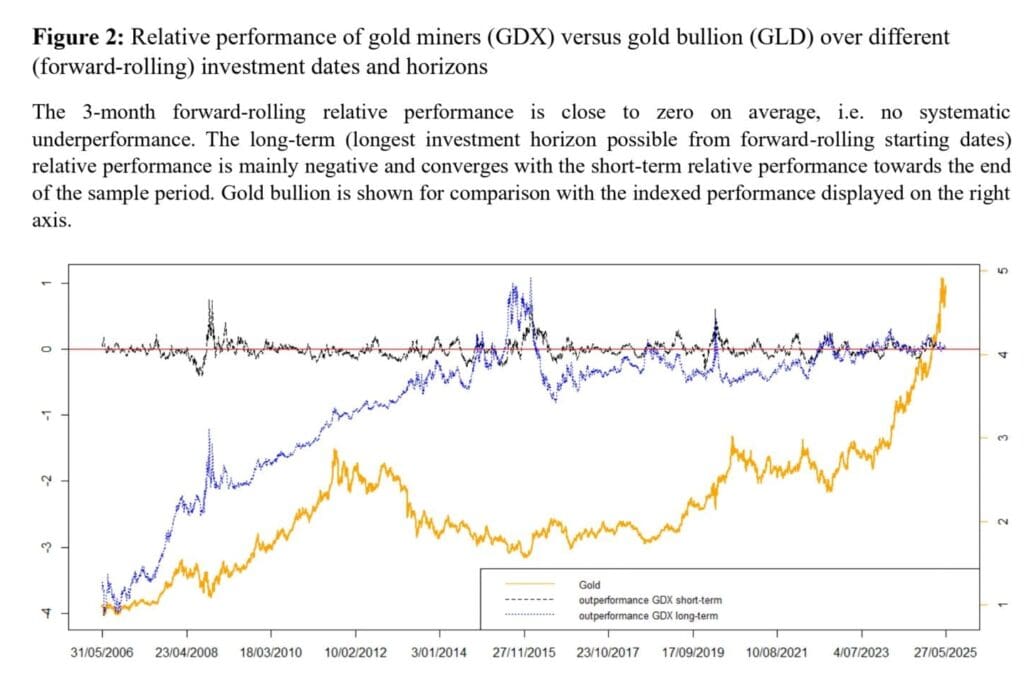

Figure 2 displays the underperformance over different time horizons, a short 3-month investment horizon and a long-term investment horizon with forward-rolling investment dates.

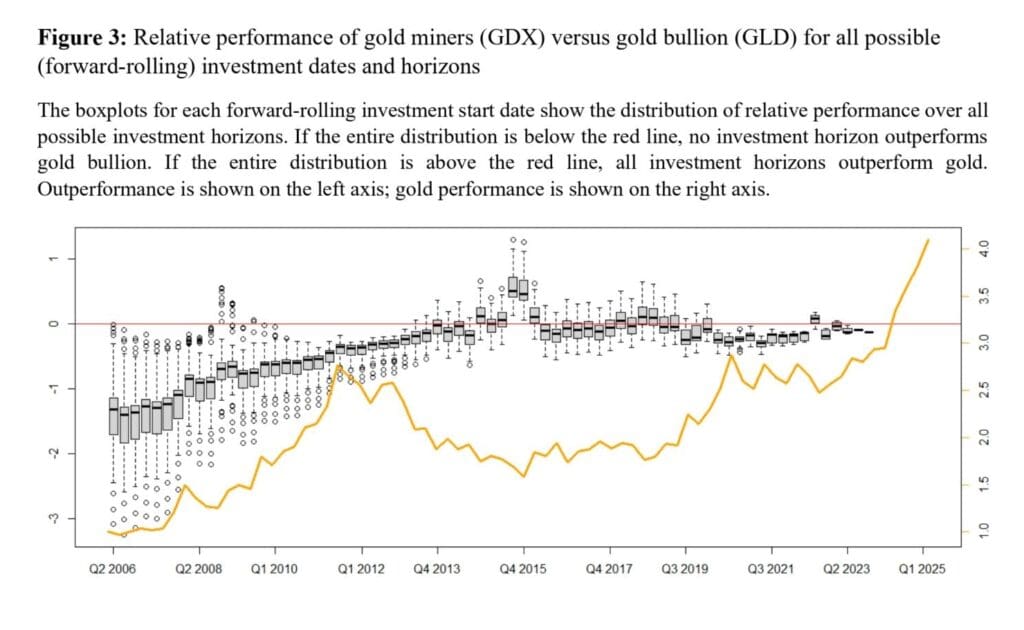

Figure 3 extends the analysis for two different investment horizons as presented in Figure 2 for all possible investment horizons based on quarterly return frequencies with boxplots. The two boxplots for investment start dates at Q3 2015 and Q4 2015 show gold miners outperformed gold for all possible horizons. No other start dates exhibit outperformance for all investment horizons.

[…] an aggregate and firm-level investment performance of gold mining companies versus gold bullion and demonstrate there is a constant negative pull on returns best explained with the finite life of mines. The finite life of mines leads to an intrinsic underperformance despite the operational leverage and other risk factors. Finally, we highlight that the potential outperformance of some mining companies due to firm-specific positive shocks (e.g., new gold discovery) is diversified away in portfolios of gold mining companies and renders such portfolios less attractive than a direct investment in gold bullion.

We conclude that the underperformance is not surprising given that mining companies are exposed to a plethora of downside technical and non-technical risks compared with gold bullion. Importantly, miners need to sustain their depleting assets and thus need to continually invest in exploration or in acquisition of new assets to maintain value. These capital expenditures and costs lead to systemic underperformance versus the gold price. Miners can, and do, also enter price-risk hedging contracts that can limit their upside gold price exposure. All such contracts also incur transaction costs. Only if gold miners had access to an “infinite” mine which would allow constant production in perpetuity would there be no requirement to replace reserves and the value of the miner could then move with the gold price, one to one or at a higher leveraged ratio, forever.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube