Fiscal stimulus measures have become a hot topic in the financial markets. However, that is not surprising, since fiscal stimulus is a crucial government method to ease the pandemic crisis’s impacts. Therefore, the investors and market are very sensitive to this topic, and they react to the fiscal stimulus and any related news very sharply. While it is intuitive that the withdraw of the stimulus measures will negatively affect the markets and markets will fall, the magnitude of these falls is unknown. Novel research by Chan-Lau and Zhao (2020), quantifies the impacts of withdrawals and it’s effects on the stock markets worldwide. The reactions are especially negative if the fiscal stimulus is withdrawn “too soon”. According to the authors, too soon is when the number of daily COVID cases is high compared to the recent past.

Authors: Jorge A. Chan-Lau and Yunhui Zhao

Title: Hang in There: Stock Market Reactions to Withdrawals of COVID-19 Stimulus Measures

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3738309

Abstract:

The COVID-19 pandemic crisis has triggered unprecedented stimulus policy responses by countries worldwide, particularly fiscal stimulus measures. Given the high fiscal costs, some countries have withdrawn such measures, and other countries are contemplating doing so. In this paper, we empirically examine the impact of the withdrawal of fiscal stimulus policies on stock markets using daily data. To this end, we construct a database of withdrawal events and examine the difference between the pre- and post-event stock price returns using event study analysis and cross-country regressions. The results show a significant negative reaction when stimulus is withdrawn prematurely, i.e., when the daily COVID cases were still high relative to the historical pattern. The results suggest that markets are concerned about the negative impact of early withdrawals of stimulus on the economic recovery prospect, a risk that policymakers need to account for while contemplating the exit strategy from the exceptional crisis-fighting policies.

As always, the results can be presented through interesting charts:

Notable quotations from the academic research paper:

“In the time of COVID-19, extending the exceptional government support measures would lead to higher fiscal costs and increase the risk that the debt burden becomes unsustainable. Yet, unwinding the measures too early may disrupt the normalization of economic activities and damage the incipient economic recovery. This analysis attempts to quantify the market views on the trade-off using a combination of event studies and cross-country regressions. The results show that markets, as proxied by the behavior of stock price returns, react negatively when government stimulus was withdrawn prematurely, that is, when the number of daily COVID-19 cases were still high relative to the recent past. In addition, we find that social unrest hurts smaller firms the most, and the problem could be compounded if reduced government support further fuels social tensions.

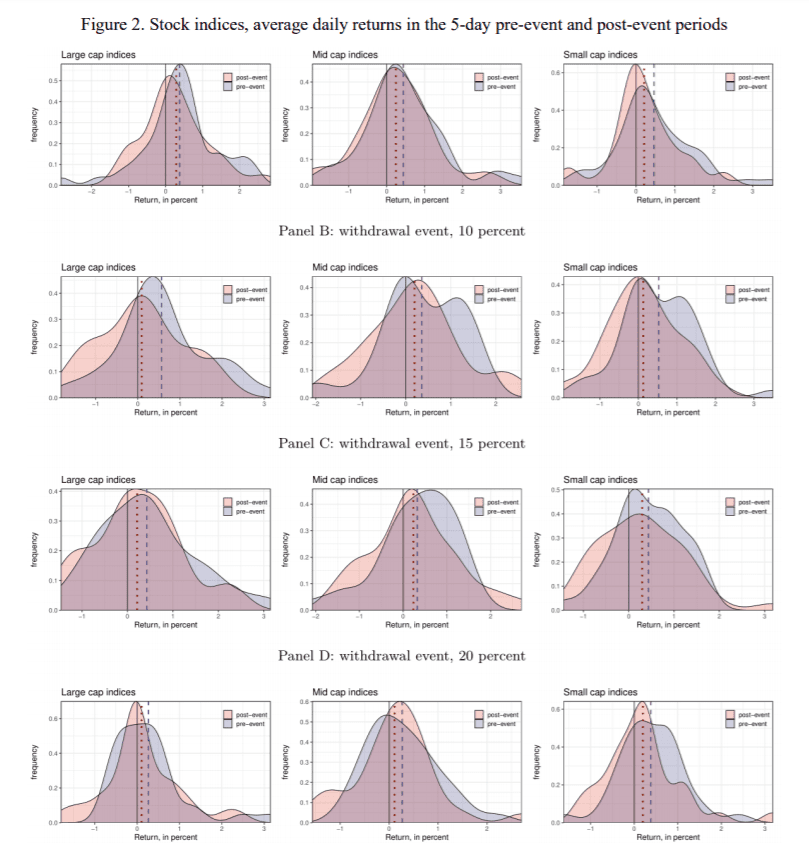

Regardless of the firm capitalization and the magnitude of the government support withdrawal, the market reaction is negative across countries. The mean difference between post-event window and pre-event window returns is negative, ranging from a minimum of -0.09 percent to a maximum of -0.5 percent. Nevertheless, the paired-sample t-tests suggest that the difference is not statistically significant in most cases. This is evident in Figure 2, which shows that the difference between pre-event and post-event return distributions is mainly concentrated on the tail behavior rather than the central section of the distribution.

In the post-event distribution, besides the leftwards shift of the mean relative to the pre-event distribution, the distribution mass tends to shift to the right reflecting lower skewness. In addition, the tails of the distribution become thinner, reflecting lower and even negative excess kurtosis.

Despite the need for further work, hereby we still lay out some policy implications to stimulate more discussions. First, it may not be wise to withdraw the fiscal support measures when the economy is not “out of the woods” yet. The pandemic experience so far, based on countries following diverse health and pandemic prevention policies, is that there could be successive infection waves as social distancing and mobility restriction measures are lifted so caution is warranted. In addition, even if policymakers are confident that there is no new COVID waves, the presence of long-lasting scarring effects would also prevent the economy from a quick recovery if the support measures were withdrawn too early.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube