Foreign exchange (FX) markets are a cornerstone of global finance, offering investors and corporations opportunities to manage currency risk, enhance returns, and optimize portfolio performance. Among the most critical challenges in FX is the design of robust hedging strategies to mitigate exposure to volatile currency movements. How does the financial industry deal with this task? We can draw inspiration from the paper written by Castro, Hamill, Harber, Harvey, and Van Hemert, which explores strategies such as dynamic hedging, trend-following, and momentum-based approaches, the concept of carry, and the interplay of these strategies with fundamental concepts like Purchasing Power Parity (PPP) and valuation metrics.

The authors set out to identify practical, return- and risk-aware ways to hedge the currency exposure that comes with international equity investing. They argue the classic “fully hedge vs. don’t hedge” framing is naïve, because hedging interacts with expected FX returns (carry), companies’ economic currency exposures, and cross-asset correlations. They therefore test dynamic hedging rules based on carry (interest-rate differentials), 12-month trend (momentum), and value (PPP deviation), and compare them with portfolio methods—a dynamic minimum-variance hedge and an “optimal” hedge that jointly optimizes equity and FX exposures. The analysis spans developed (and some emerging) markets from the post-Bretton Woods era to June 2024, using forwards or synthetic forward returns, and evaluates both single-market and a world-equity basket perspective.

They hypothesize that conditioning the hedge on information (carry/trend/value) and accounting for covariances should beat static hedging on risk-adjusted performance and behave more sensibly across regimes (crises vs. calm; inflationary vs. non-inflationary). They also tackle practical problems: (i) full hedging doesn’t necessarily minimize risk because firms’ revenues/costs are multi-currency; (ii) decisions often ignore expected returns like carry; (iii) the hedge for one country should depend on others via correlations; and (iv) investors need approaches that remain robust in crises and inflation bursts. Hence the exploration of dynamic min-vol and a constrained optimal hedge that fixes equity weights and chooses currency hedge ratios given expected FX returns (carry) and a rich covariance structure.

Main findings

- Static rules leave money on the table. Simple dynamic approaches consistently improve performance relative to fully-hedged or unhedged baselines.

- Carry is powerful for hedging decisions. When the interest-rate differential is positive, FX returns are higher; when negative, FX returns are negative—guiding a “Max Carry” rule that outperforms static hedging in almost every developed market perspective.Country specifics match intuition.

- Low-rate home currencies (e.g., JPY) historically benefit from staying unhedged (+180 bps vs. hedged), while high-rate homes (e.g., NZD) benefit from hedging (~+100 bps p.a.).

- Momentum and value add. A 12-month trend signal and PPP-based value each help time the hedge; both are useful complements to carry.

- Dynamic Min-Vol works as intended. A covariance-aware, volatility-minimizing hedge generally delivers lower realized volatility than either static hedged or unhedged portfolios, and often improves Sharpe.

- “Optimal” hedging (carry as expected FX return + full covariance) is frequently best. With a reasonable risk-aversion setting, it achieves the top Sharpe in most developed markets (e.g., 9 out of the sample’s DMs).

- Regime robustness. In equity crises, fully-hedged can be worst; carry does not systematically blow up, and Min-Vol often cushions losses best. In inflationary periods, dynamic rules (especially carry) typically beat static hedged/unhedged.

- Caveats. EM history is shorter and subject to survivorship effects; results rely on forwards/synthetic forwards and stitched euro histories.

Authors: Pedro Castro et al.

Title: The Best Strategies for FX Hedging

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5047797

Abstract:

The question of whether, when, and how to hedge foreign exchange risk has been a vexing one for investors since the end of the Bretton Woods system in 1973. Our study provides a comprehensive empirical analysis of dynamic FX hedging strategies over several decades, examining various domestic and foreign currency pairs. While traditional approaches often focus on risk mitigation, we explore the broader implications for expected returns, highlighting the interplay between hedging and strategies such as the carry trade. Our findings reveal that incorporating additional factors-such as trend (12-month FX return), value (deviation from purchasing power parity), and carry (interest rate differential) – into hedging decisions delivers significant portfolio benefits. By adopting a dynamic, active approach to FX hedging, investors can enhance returns and manage risk more effectively than with static hedged or unhedged strategies.

As always, we present several interesting figures and tables:

Notable quotations from the academic research paper:

“[A] binary and static framing of the question ‘to hedge or not to hedge’ is naïve for a number of reasons.1 First, fully hedging FX risk may not minimize risk. The returns of an asset one seeks to hedge may be influenced by changes in exchange rates, even when those returns are expressed in the local currency. For example, the revenues of stocks in an equity index may be partially earned in a foreign currency. Similarly, input prices may be impacted by foreign exchange rate movements. For example, the FTSE100 index of the largest U.K. stocks will have FX exposures because global businesses inevitably derive their earnings in a range of different currencies.

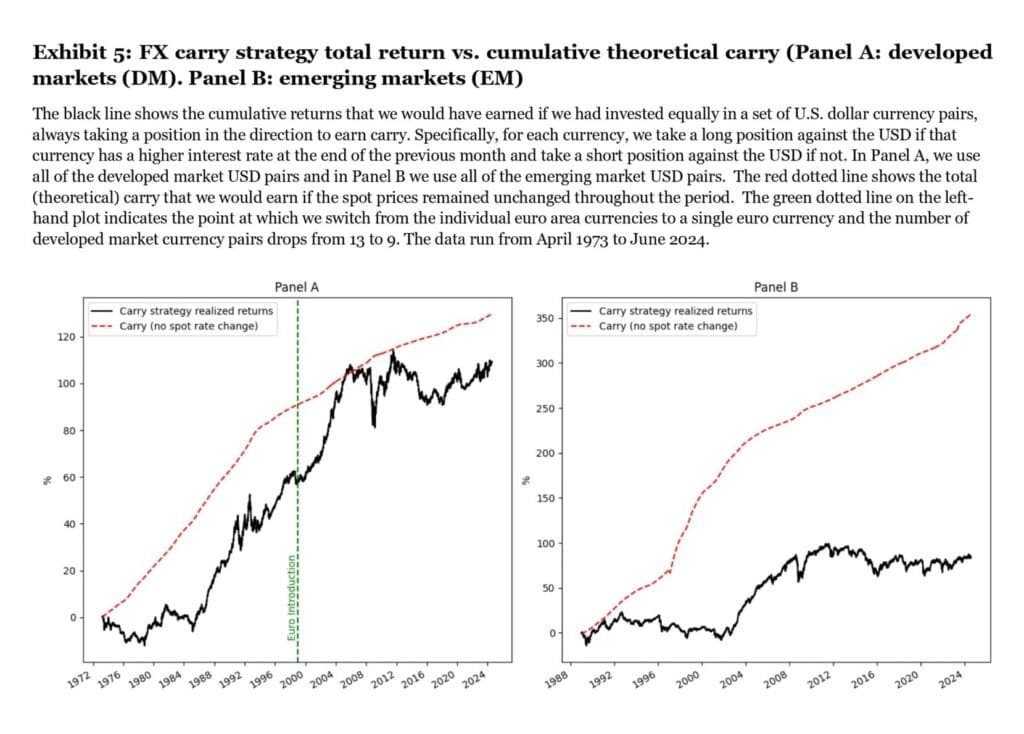

In Exhibit 5, we create a simple FX strategy that trades each of the developed market FX currencies against the U.S. dollar on an equally weighted basis. In this initial analysis, we are not taking portfolio considerations into account. That is, we treat each currency pair independently. If a currency has a higher interest rate than the U.S. in the previous month, we take a long position in that currency against the US dollar for the subsequent month; if not, we take a short position. As such, the strategy is always positioned to earn carry.

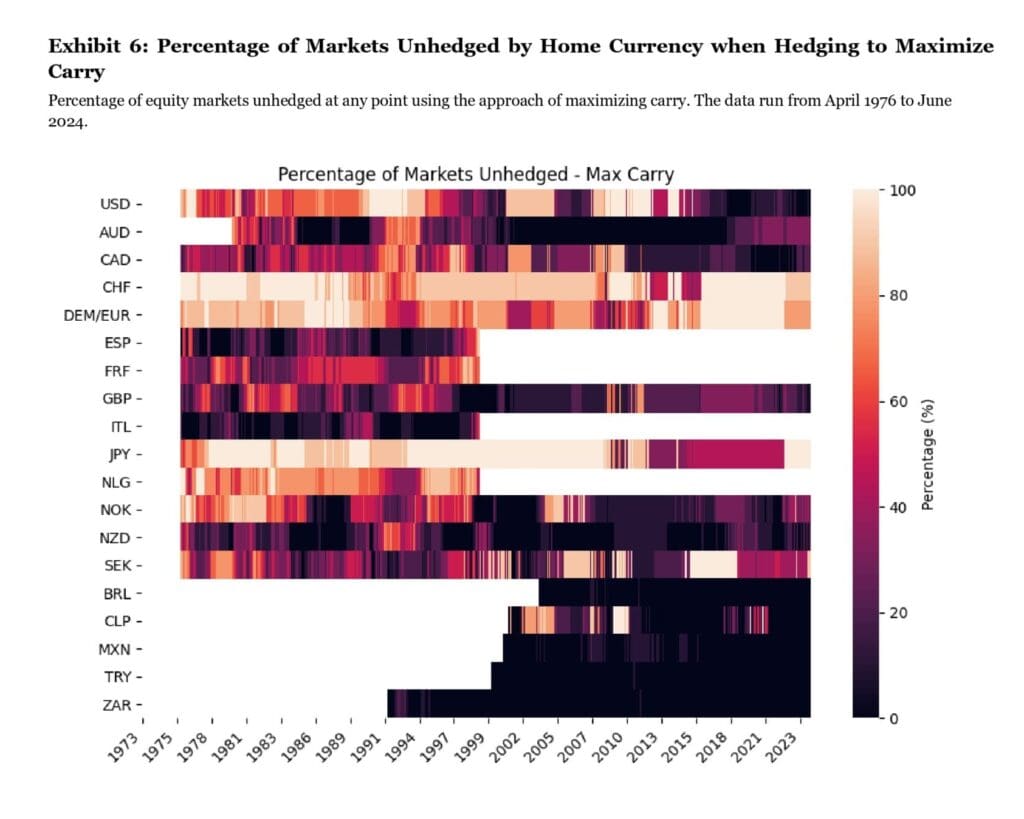

The final column in Exhibit 4 implements a dynamic hedging approach which we label as “Max Carry”.12 With this strategy, if the interest rate differential (equity market currency minus home currency) is positive, then there is no hedging. When the differential is negative, the investor will hedge the FX. The results in column 6 show that the max carry approach dominates the static strategies across the 14 developed markets. In nine of the 14 markets, the improvement over full static hedging exceeds 100bps per year. The proportion of markets unhedged through time is presented in Exhibit 6.

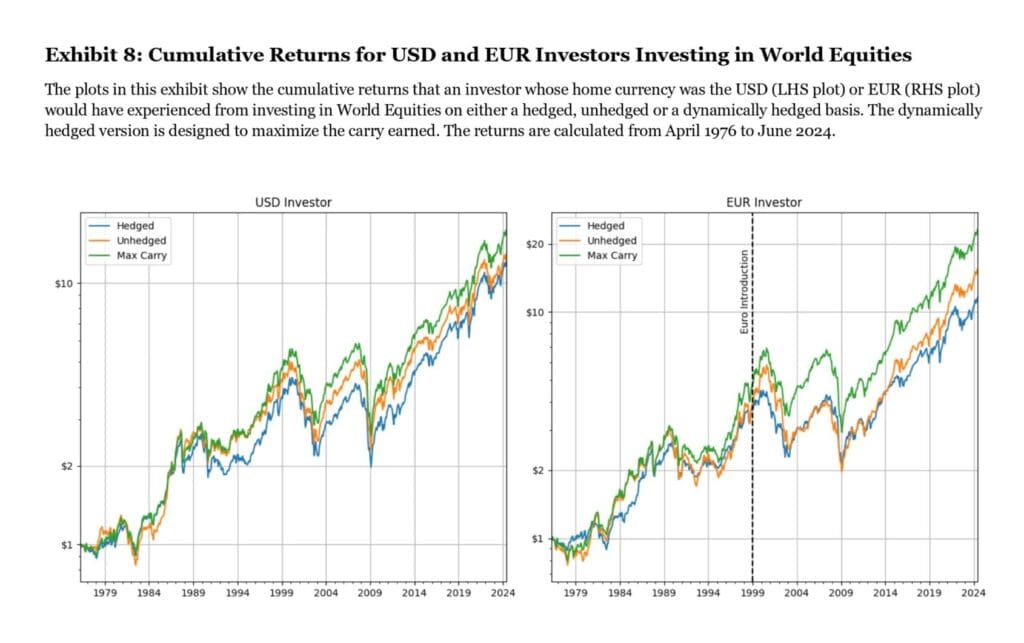

The cumulative returns from the perspective of a U.S. dollar investor as well as a euro-based investor are presented in Exhibit 8. The Max Carry strategy is consistently the highest in terms of excess returns. Furthermore, the strategy continues to do well after the introduction of the Euro in 1999.

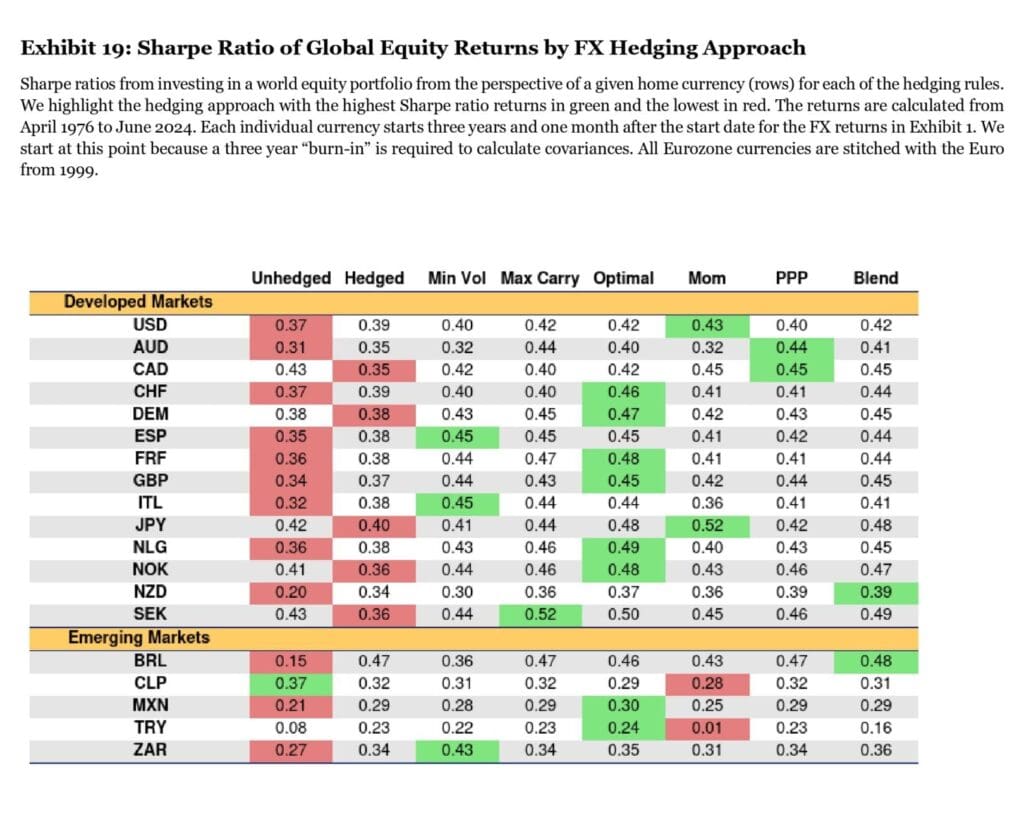

In Exhibit 19, we show the Sharpe ratios that would have been realized by investors in different home currencies from investing in a basket of global equities.26 Notice that in every developed market the lowest performers are the static unhedged or fully hedged. The dynamic approaches show distinct advantages. Even with these relatively simple formulations, both the PPP approach and the momentum approach show reasonable promise. The PPP hedging rule outperforms both the hedged and unhedged version in all but one of the developed market currencies and the momentum rule outperforms in 12 of the 14 developed markets. Furthermore, in a number of markets, either the PPP rule or the momentum rule generate the highest Sharpe ratio, suggesting that both value and momentum may be additive to our existing rules.”

Are you looking for more strategies to read about? Sign up for our newsletter or visit our Blog or Screener.

Do you want to learn more about Quantpedia Premium service? Check how Quantpedia works, our mission and Premium pricing offer.

Do you want to learn more about Quantpedia Pro service? Check its description, watch videos, review reporting capabilities and visit our pricing offer.

Are you looking for historical data or backtesting platforms? Check our list of Algo Trading Discounts.

Would you like free access to our services? Then, open an account with Lightspeed and enjoy one year of Quantpedia Premium at no cost.

Or follow us on:

Facebook Group, Facebook Page, Twitter, Linkedin, Medium or Youtube